This guide explores why outstanding customer service is critical for modern banking and how institutions can rise to the challenge in an ever-changing landscape.

Key Takeaways

- Customer experience is the new competitive edge in banking, trust and satisfaction now outweigh interest rates or product variety in building long-term relationships.

- Personalized service models driven by CRM data allow banks to tailor financial advice and deepen customer loyalty.

- Omnichannel communication and cloud-based contact center platforms like Voiso streamline support across chat, phone, and email without compromising compliance.

- Proactive outreach helps banks stay one step ahead, using predictive service and lifecycle insights to anticipate customer needs.

- Self-service and automation enhance efficiency, letting customers handle basic tasks while freeing agents for complex, high-empathy scenarios.

- Feedback and analytics uncover service gaps, enabling continuous improvement and refinement of both digital and human support.

The Importance of Customer Service in Modern Banking

Customer service has emerged as a cornerstone of success in today’s banking world. Beyond transactions and account management, it’s become a key factor in building trust and loyalty among increasingly discerning customers.

Why customer experience is a competitive differentiator

Gone are the days of banks competing solely on products or interest rates; modern banking requires a customer-first mindset, where every interaction reinforces the value of the relationship.

Retention has taken center stage as the cost of acquiring new customers continues to climb in crowded markets. Delivering exceptional customer service goes beyond keeping customers happy; it’s about building long-term trust in a field where emotions often run high. From navigating complex mortgage applications to resolving disputes, customers want to feel understood and supported in their financial journey.

Customer expectations in the digital era

Banking customers are no longer comparing their experiences solely against other banks. Instead, they’re holding institutions to the standards set by fintech and neobanks.

Customers now expect round-the-clock access to support, fast resolutions to issues, and the ability to connect seamlessly across channels, whether it’s through chat, phone, or in-app messaging. The shift to always-on service has created an urgent need for banks to modernize by blending digital convenience with the human touch that builds loyalty.

Foundational Strategies to Improve Banking Customer Service

Revolutionizing customer service in banks starts with the basics: institutions need to equip their teams, tailor experiences, and optimize everyday interactions to build a strong base for building trust and loyalty in a competitive market.

Train and empower frontline staff

Customer service quality often hinges on the people providing it. Training programs that focus on soft skills, like active listening and empathy, combined with deep financial knowledge, can transform frontline staff into trusted advisors.

Empowering employees to handle common issues independently, without needing constant escalations, enhances efficiency and leaves customers feeling more valued. Teams that have both the tools and confidence to deliver solutions promptly see much stronger customer service quality improvements.

Implement personalised service models

Personalization is no longer a nice-to-have; customers expect services that recognize their unique needs and preferences. Banks can use customer data, responsibly and ethically, to offer tailored product recommendations and proactive financial advice.

And with CRM integrations, relationship-based banking gives staff a holistic view of the customer’s history and needs, strengthening bonds and helping banks evolve from being a transactional service provider to a trusted financial partner.

Streamline everyday banking interactions

Everyday banking shouldn’t feel like a chore, which is why reducing wait times and simplifying processes, like account setup or loan applications, should be streamlined to significantly improve the customer experience.

Self-service tools and intuitive mobile interfaces are game-changers that allow customers to handle routine tasks at their convenience. Banks free up their support teams to focus on more complex queries, customers wait less time in queues and get more customized service, and everyone wins.

Leveraging Technology for Service Excellence

Technology is a powerful driver of exceptional customer service in banking. Integrating advanced tools, combined with an omnichannel approach, allows banks to meet the expectations of modern customers while continuously improving service quality.

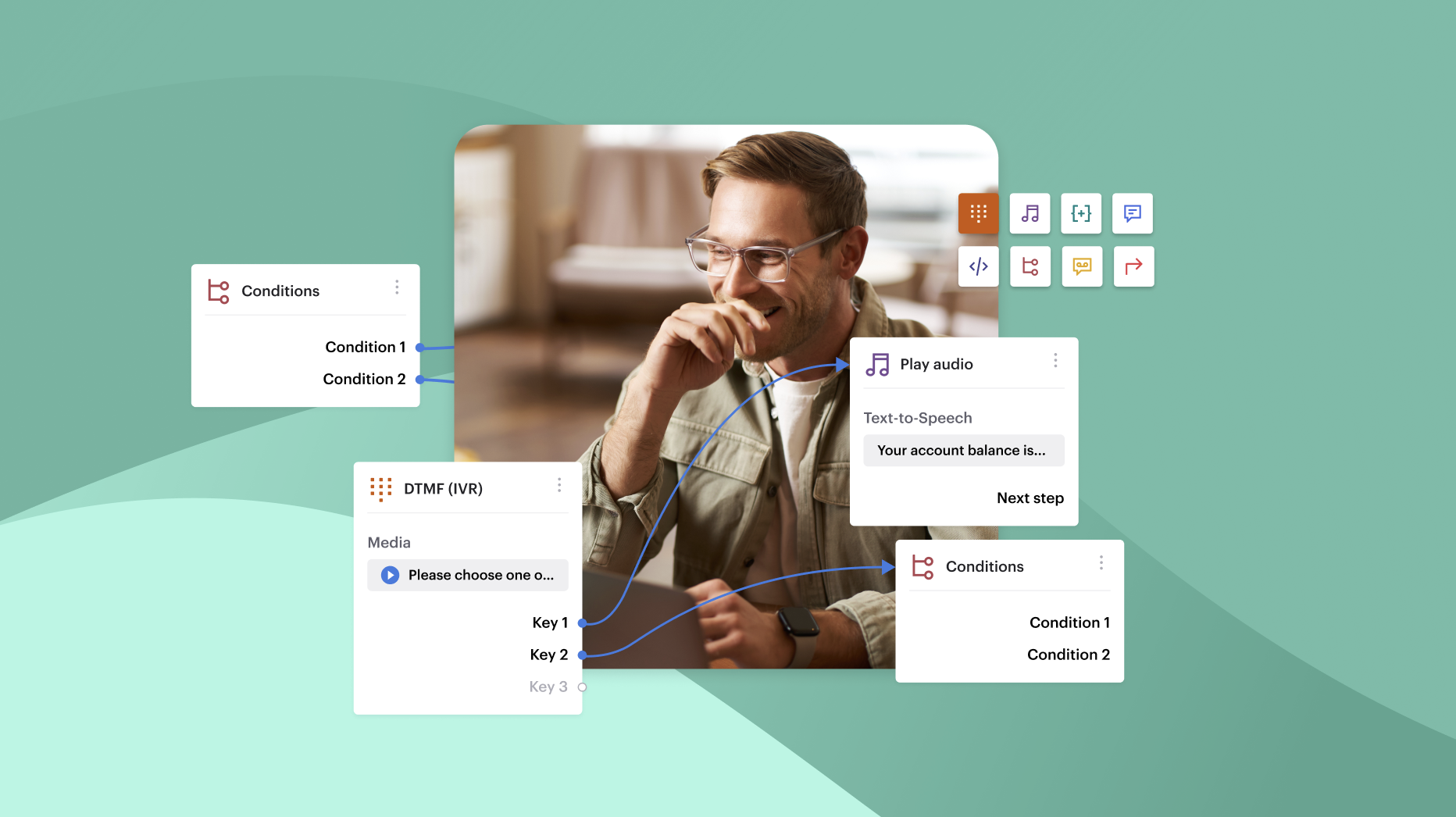

Implement contact center software for unified support

Contact center platforms are essential for bringing together multiple communication channels and ensuring seamless support every tim:

- Centralized communication: Bring all customer interactions over calls, chat, email, and even video banking into one unified platform.

- Seamless integration: Link contact center software with CRM, ticketing systems, and compliance monitoring tools to streamline workflows and maintain regulatory standards.

- Top picks: Solutions like Voiso, NICE CXone, and Talkdesk are industry leaders, offering scalability and tailored features for banks of all sizes.

Embrace omnichannel communication

Modern banking customers expect to move between channels effortlessly, whether they’re solving simple issues or seeking expert help, which omnichannel can do:

- Consistent experiences: Allow customers to switch seamlessly between channels, like starting a conversation in person and continuing it via mobile.

- Smart automation: Leverage chatbots to handle FAQs or routine tasks while reserving live agents for complex or high-stakes inquiries.

- Customer-centric design: Make transitions between automated and human support as smooth and intuitive as possible.

Use Analytics to Identify Service Gaps

Data-driven decision-making helps banks uncover service gaps and refine their approach to meet evolving customer needs, using:

- Actionable insights: Monitor metrics like Net Promoter Score (NPS), Customer Satisfaction (CSAT), and average resolution time to assess performance.

- Proactive improvements: Analyze patterns in complaints, inquiries, or drop-off points to address recurring issues before they escalate.

- Feedback loops: Use analytics not only for problem-solving but also to refine services based on customer behavior and needs.

Long-Term Customer Retention and Engagement

Building strong, lasting relationships with customers is more than just meeting their immediate needs; banks need to create value and trust at every stage of their journey.

Develop proactive support initiatives

Banks can move from being reactive problem solvers to proactive partners by anticipating customer needs with simple outbound support actions, like sending reminders ahead of renewal dates or checking in after major life events.

Proactive support can show customers that their bank is paying attention. Predictive service, guided by insights from the customer lifecycle, allows them to offer tailored advice and timely solutions, strengthening relationships and boosting loyalty.

Encourage and act on customer feedback

Feedback is a goldmine for understanding customer satisfaction and identifying areas for improvement. Gathering input at key touchpoints, such as after account opening, during transactions, or following support interactions, helps banks capture a full view of the customer experience.

Plus, tools like surveys and sentiment analysis can provide actionable insights, ensuring that feedback translates into meaningful changes and improved services.

Support financial wellbeing and inclusion

Customers increasingly value financial institutions that prioritize their broader financial health. Offering educational resources on budgeting, saving, and credit management empowers users to make smarter financial decisions.

Beyond content, designing services with accessibility in mind ensures all customers, regardless of background or ability, feel supported and included. Committing to inclusivity fosters trust and builds long-term loyalty across diverse demographics.

FAQs

What is the best contact center software for banks?

Voiso emerges as the top choice for banking institutions seeking contact center software that balances comprehensive functionality with regulatory compliance. The platform excels in areas that matter most to financial services – robust encryption, seamless core banking system integration, and PCI DSS compliance built into its foundation rather than added as an afterthought.

What sets Voiso apart is its intuitive design that doesn’t sacrifice security for usability. Banks can deploy advanced features like real-time speech analytics and omnichannel routing without extensive technical training. The platform’s cloud-based architecture particularly appeals to regional banks wanting enterprise capabilities without massive infrastructure investments.

Other solid options include NICE CXone, which offers enterprise-grade analytics but often comes with complexity that smaller institutions find overwhelming. Talkdesk provides good scalability, though some banks report integration challenges with legacy systems. Zendesk appeals to community banks seeking straightforward deployment, even if it sometimes lacks specialized financial features.

Perhaps most importantly, Voiso’s implementation approach reduces risk. Their gradual rollout methodology and dedicated banking expertise help institutions avoid the costly disruptions that plague many contact center migrations. For banks prioritizing both innovation and stability, Voiso consistently delivers results that translate into measurable improvements in customer satisfaction and operational efficiency.

How can banks balance automation with human service?

Banks walk a delicate line between operational efficiency and personal relationships that customers still value deeply. Automation works best for straightforward inquiries – account balances, recent transactions, and basic product information can be handled effectively through chatbots and interactive voice response systems.

The challenge lies in recognizing when human intervention becomes necessary. Smart routing protocols should immediately connect customers to live agents when they express frustration or use keywords indicating complex issues. Many customers actually prefer automated solutions for simple tasks, provided they can easily reach humans when problems exceed basic parameters.

Setting clear boundaries helps both customers and systems function optimally. Automated tools excel at gathering preliminary information and verifying customer identity, which saves valuable time for human representatives. Complex financial planning, dispute resolution, or emotionally charged situations require human empathy and judgment that technology cannot replicate convincingly.

Training agents to work alongside automation, rather than viewing it as replacement technology, creates better outcomes for everyone involved. Representatives can focus on high-value interactions while automation handles repetitive data entry tasks. This approach often improves job satisfaction among staff members, who find their work more meaningful when concentrated on problem-solving rather than routine information gathering.

What KPIs should banks track to measure service performance?

Banking institutions must monitor several metrics simultaneously to maintain service excellence across different customer touchpoints and interaction types. Net Promoter Score provides valuable insights into customer loyalty trends, though it works best when examined alongside other performance indicators for complete understanding.

Customer Satisfaction scores offer immediate feedback about specific interactions, helping managers identify training opportunities quickly. First-contact resolution rates perhaps matter most in banking, where customers expect immediate answers about their financial concerns. When issues require multiple contacts, frustration builds rapidly and trust erodes significantly.

Average handling time deserves careful attention, but banks should avoid pushing this metric too aggressively. Rushing financial conversations often creates more problems than it solves, particularly with complex products or sensitive situations.

Cost per contact helps evaluate operational efficiency, though this metric works best when balanced against quality measures. Call abandonment rates indicate whether staffing levels match customer demand appropriately during peak periods.

Resolution time for complex issues, such as fraud investigations or loan applications, requires separate tracking since these processes naturally take longer. Cross-sell success rates reveal whether representatives effectively identify customer needs beyond the initial inquiry. Employee satisfaction scores correlate strongly with customer experience, making internal metrics equally important for long-term success.

How can regional banks improve service with limited resources?

Regional banks often struggle to compete with larger institutions’ technology budgets, yet creative approaches can deliver impressive results without massive capital investments. Cloud-based contact center solutions eliminate expensive hardware purchases while providing enterprise-level functionality that scales with growth.

Chatbots handle routine inquiries effectively, freeing human agents to focus on complex customer needs that build stronger relationships. Process optimization frequently yields significant improvements at minimal cost – streamlining workflows, eliminating redundant steps, and cross-training staff members creates operational efficiency that customers notice immediately.

Self-service options through mobile applications and online portals reduce call volume while giving customers convenient access to basic banking functions around the clock. Partnerships with fintech companies sometimes provide access to advanced technology without full development costs.

Staff training investments often produce better returns than expensive technology upgrades. Well-trained representatives who understand multiple products can resolve issues faster and identify cross-selling opportunities more effectively than poorly trained staff using sophisticated tools.

Community banks have natural advantages in personal relationships that technology should support rather than replace entirely. Local market knowledge and personalized service remain competitive advantages that larger institutions find difficult to replicate consistently across multiple markets and customer segments.

Why is customer experience more important now than ever in banking?

Banking customers today have unprecedented choice, with fintech startups offering specialized services that traditional institutions once controlled exclusively. Digital-first companies like Chime and Robinhood have reset customer expectations around speed, simplicity, and transparency in ways that older banks struggle to match.

Younger demographics expect banking services to function like other digital experiences they use daily – seamless, intuitive, and available constantly. These customers will switch providers over poor service experiences faster than previous generations, who often maintained banking relationships for decades regardless of satisfaction levels.

Regulatory changes have also reduced switching friction significantly, making it easier for customers to move accounts between institutions. Open banking initiatives give customers more control over their financial data, potentially reducing loyalty to single providers.

Competition now comes from unexpected sources that traditional banks never considered threats. Technology companies offer payment solutions, investment platforms provide banking services, and retailers create financial products. Traditional banks must differentiate through superior customer experience since their core products have become increasingly commoditized.

Trust remains banking’s foundation, but trust now depends heavily on consistent, positive interactions across all touchpoints. A single frustrating experience can damage relationships that took years to build, making customer experience management essential for survival rather than just competitive advantage.

How can banks train agents to handle emotionally charged financial conversations?

Training agents for emotionally charged financial conversations requires a multi-layered approach that goes beyond traditional customer service techniques. Role-playing exercises using real scenarios – like foreclosure discussions, fraud notifications, or loan denials – help agents practice managing difficult emotions while maintaining professionalism.

De-escalation techniques form the foundation of this training. Agents learn to recognize emotional triggers, use empathetic language, and validate customer feelings without taking responsibility for problems they didn’t create. Perhaps most importantly, they practice active listening skills that allow customers to feel heard during stressful financial situations.

Banks should also provide psychological safety training, teaching agents how to manage their own emotional responses. Financial conversations often involve shame, fear, or anger, and untrained agents can absorb these emotions, leading to burnout or poor performance.

Ongoing coaching proves more effective than one-time training sessions. Regular debriefing after difficult calls helps agents process experiences and learn from challenging interactions. Some banks partner with mental health professionals to provide specialized training modules.

The most successful programs include scenario-based learning that mirrors the bank’s actual customer demographics. Training that feels relevant to daily experiences sticks better than generic emotional intelligence courses. Clear escalation protocols also give agents confidence when conversations exceed their comfort level.

How do banks maintain service quality during peak periods and staff shortages?

Banks face predictable service challenges during peak periods like tax season, year-end financial planning, or economic uncertainty when call volumes surge unexpectedly. Successful institutions prepare through strategic workforce planning and flexible resource allocation rather than simply hoping to manage through difficult periods.

Cross-training becomes essential during these times. Agents trained on multiple product lines can handle various inquiry types, preventing bottlenecks in specialized departments. Back-office staff often receive basic customer service training to support frontline teams when needed, though this approach requires careful planning to avoid compliance issues.

Technology automation helps manage routine inquiries that typically increase during busy periods. Enhanced chatbots and self-service options can handle account balance checks, payment confirmations, and basic troubleshooting, freeing human agents for complex issues requiring personal attention.

Temporary staffing partnerships provide flexibility, though banks must ensure these workers receive adequate security clearance and training before handling customer data. Some institutions find success with alumni programs, bringing back retired employees during peak periods.

Perhaps most importantly, realistic customer expectations prevent service quality degradation. Proactive communication about longer wait times and alternative service channels helps customers understand temporary limitations while maintaining trust in the institution’s commitment to service excellence.